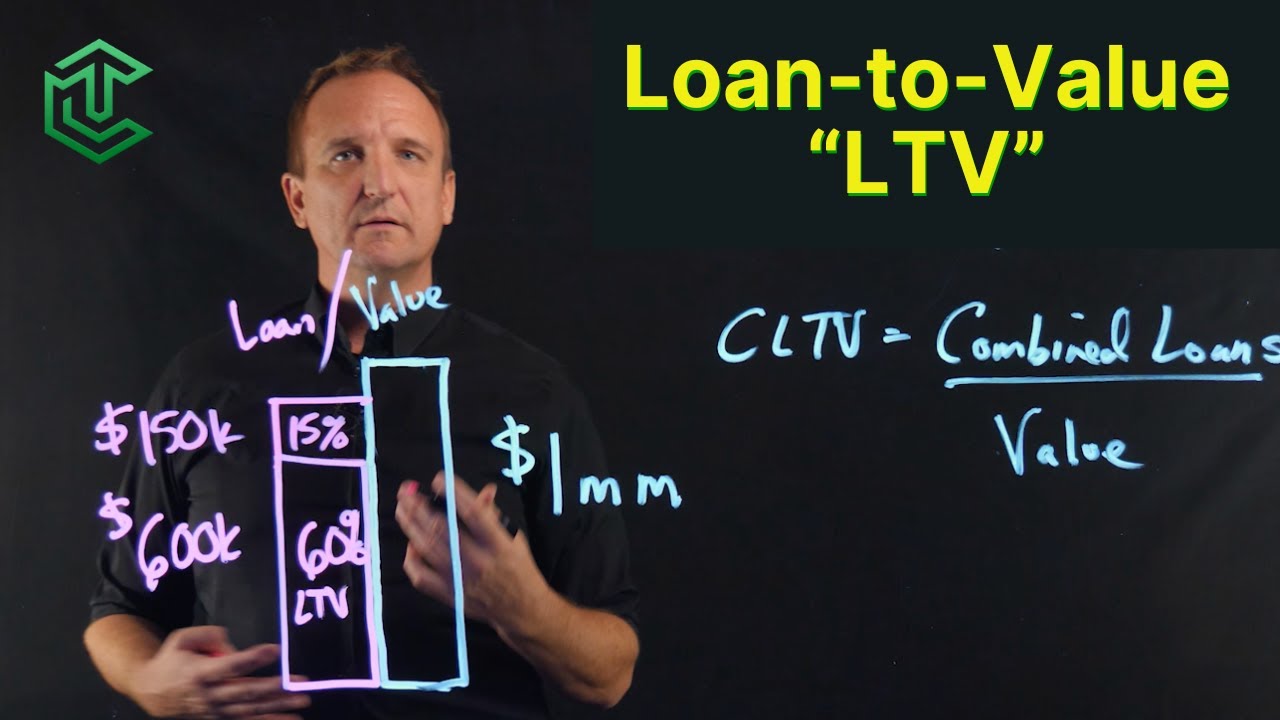

If you are looking for the exact answer to this common real estate question: If the loan-to-value (LTV) were 90% for a $200,000 home, the required down payment would be $20,000.

The math behind this calculation is straightforward. A 90% Loan-to-Value ratio means the lender is financing 90% of the property’s total purchase price. As the buyer, you are responsible for covering the remaining 10% upfront.

Here is the exact breakdown:

| Metric | Calculation | Amount |

| Home Purchase Price | Base value | $200,000 |

| Loan Amount (90% LTV) | $200,000 × 0.90 | $180,000 |

| Required Down Payment | $200,000 – $180,000 | $20,000 |

What is a Loan-to-Value (LTV) Ratio?

In real estate and mortgage lending, the Loan-to-Value (LTV) ratio is a financial term used by lenders to express the ratio of a loan to the value of an asset purchased.

Banks and mortgage companies use this metric to assess risk. A higher LTV (like 90% or 95%) represents a higher risk for the lender, which is why loans with an LTV over 80% typically require the homebuyer to purchase Private Mortgage Insurance (PMI).

The Standard LTV Formula

To calculate the LTV yourself, you can use this simple formula: LTV Ratio = (Mortgage Amount / Appraised Property Value) × 100

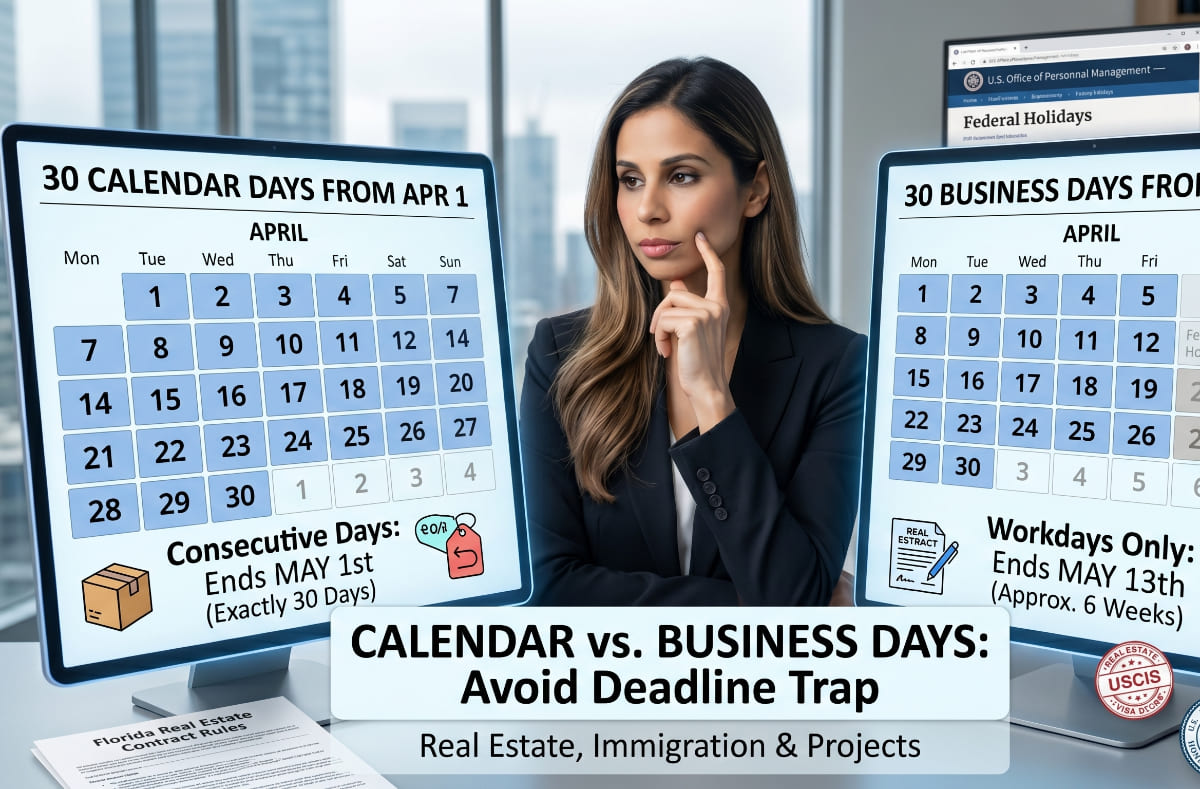

How Long Does a Mortgage Take to Close? (Business Days Timeline)

Once you have your $20,000 down payment ready for your 90% LTV loan, the next critical question is timeline. Securing mortgage approval isn’t an overnight process.

On average, it takes between 30 to 45 calendar days to close on a house. However, financial institutions operate strictly on business days (excluding weekends and federal holidays).

Here is a realistic business day timeline for processing a mortgage:

- Initial Underwriting: 3 to 5 business days.

- Property Appraisal: 5 to 10 business days (depending on market demand).

- Conditional Approval to Clear-to-Close: 10 to 15 business days.

- Closing Disclosure (CD) Review Period: By federal law, lenders must give you exactly 3 business days to review your CD before you can sign the final paperwork.

When planning your move, counting standard calendar days can lead to scheduling disasters with your moving company. A 45-calendar-day closing period usually translates to roughly 31 to 32 actual business days, depending on upcoming federal holidays like Labor Day or Thanksgiving.

Pro Tip: Don’t guess your closing date. Use our exact Business Days Calculator to determine your precise closing window by excluding weekends and US federal holidays.

Key Takeaways for Homebuyers

- A 90% LTV on a $200k property always results in a $180k mortgage and a $20k down payment.

- Be prepared for extra costs: 90% LTV loans usually require PMI until you reach 20% equity.

- Always calculate your real estate deadlines using business days, not calendar days, to avoid contract breaches.